Global commercial insurance rates have turned negative for the first time in seven years. The transition from a hard market to a soft market has arrived faster than expected. Alongside this change are adverse claims trends that are likely to deteriorate reserves held for many classes of business. This was highlighted in the Q2 2026 Lloyd’s market bulletin. Therefore, Insurance carriers face a growing challenge in 2026: maintaining profitability while meeting evolving regulatory expectations. What is driving the shift and how should carriers respond?

Rates are falling faster than expected leading to a bifurcated market

The data from brokers is conclusive. The Marsh Global Insurance Market Index (GIMI) shows commercial insurance rates peaked at +22% in Q4 2020 and have declined in every subsequent quarter, turning negative in Q3 2024 and reaching −4% by Q4 2025. The Council of Insurance Agents and Brokers (CIAB) survey corroborates the trend, with its composite at +1.6% by Q3 2025 dropping from +12% during Q4 2024 —the lowest since the hard market began. Likewise, the Guy Carpenter Property CAT Rate-on-line Index Is down 12% at January 2026 renewals. The transition from peak pricing to negative rates took just four quarters. In the previous soft market cycle (2014 to 2017), the equivalent decline took eight to ten quarters. The current softening is happening at approximately twice the pace of the last cycle.

The pace of softening varies by class

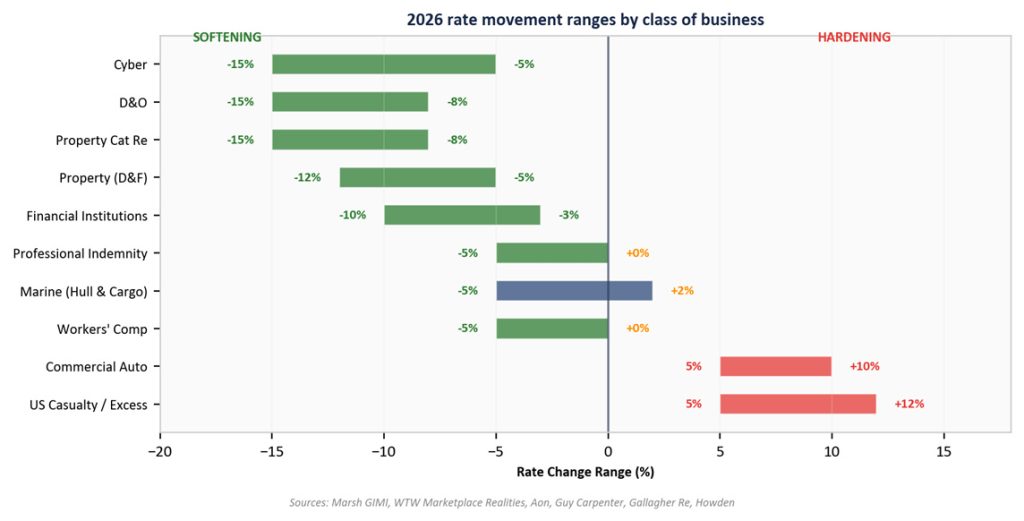

While the headline composite is negative, the picture varies dramatically by class. Property (re)insurance, cyber, financial lines and D&O are experiencing rate reductions of −15% to −3%, driven by abundant capacity and improving loss ratios. In contrast, US casualty (+5% to +12%) and commercial auto (+5% to +10%) continue to harden, reflecting social inflation and nuclear verdicts. Carriers with portfolios weighted towards property and financial lines face immediate margin pressure whereas those with US casualty exposure will have the challenge of maintaining underwriting discipline against competitive pressure as the capital supply increases in the future from new inflows and portfolio rebalancing.

What is driving the softening?

The softening (and the speed of this pricing transition) is due to the unusual convergence of several capital and capacity factors acting in the same direction simultaneously, including high retained earnings from the hard market, increased availability of alternative capital, an increase in new entrants, rising investment income from high interest rates and the low levels of CAT losses during 2023.

Key indicators of capacity from different brokers underscore the structural oversupply of capital. Reinsurance capital is at record levels – $785 billion, a 9% year-on-year increase (Aon). The Cat bond market is at an all-time high – more than $52 billion outstanding (Artemis / Aon Securities). Likewise, the Lloyd’s capacity expansion is evident from the increase in gross written premium up from £35.5 billion to £57 billion. The industry effectively over-capitalised itself during the hard market, and the resulting surplus is now compressing pricing at an accelerated pace.

Why should this concern insurance carriers?

The softening is occurring against a backdrop of deteriorating loss trends, thinning reserve margins, and heightened geopolitical risk. This may have knock on impacts on profitability and capital adequacy in the medium term, increasing scrutiny from audit and assurance functions and regulators.

- Social inflation and large US liability judgments: Nuclear verdicts (US jury awards exceeding $10 million) surged to $135 million in 2024 – a 52% year-on-year increase. The median award has grown from $21 million in 2020 to $51 million in 2024 (Marathon Strategies research). Third-party litigation funding has exceeded $20 billion based on industry estimates (Swiss Re). Therefore, the US casualty loss costs are running eight to 12 percentage points above general economic inflation (AM Best). The increase in estimates following the US Baltimore Bridge judgement is indicative of this trend.

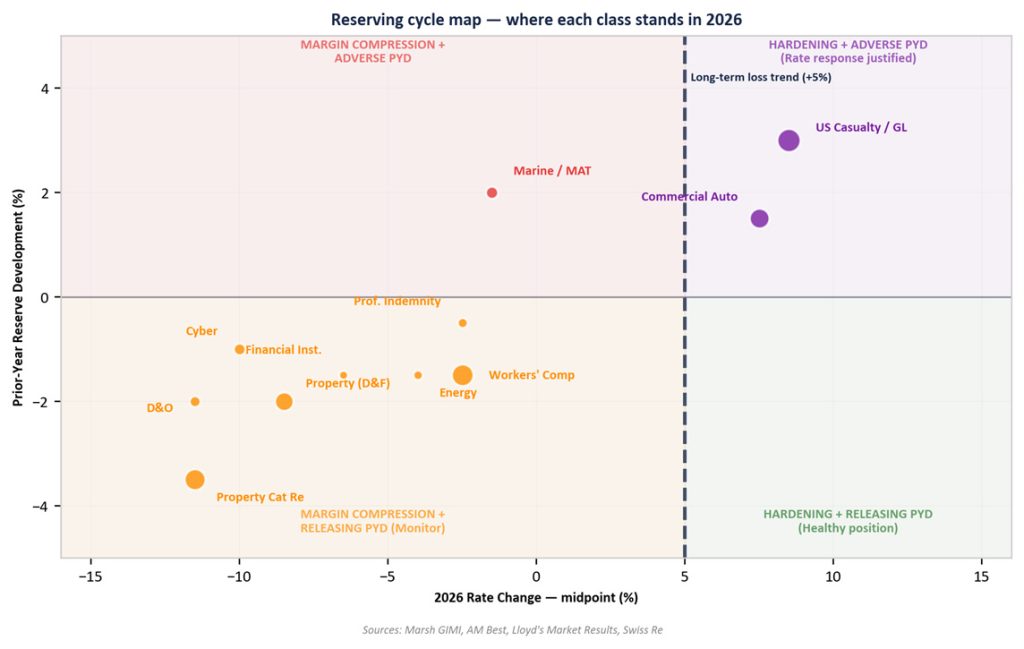

- Reserve margins are shrinking Property (re)insurance and financial lines have generated favourable prior-year development of −2% to −4% per year (AM Best). However, these are the classes where rates are softening most aggressively. On the other side of the ledger, casualty reserves are deteriorating; for example, general liability has experienced adverse development of +3.0% to +3.5% per year since 2022. Lloyd’s total reserve margin stood at £5.4 billion at the end of 2024. However, the classes generating favourable releases have decreased recently and/or are facing softening rates.

- Risk blind spots: Lloyd’s bulletin warns about changing risk landscape of Cyber risks with the emergence of AI. There is need for caution regarding coverage creep, especially liability risks and potential for catastrophe claims. Although 2025 was a relatively good outlier with regards to natural and man-made catastrophes, the long-term trend shows an increase. Insured catastrophe losses have averaged $114 billion per year (2020 to 2024), up from $75 billion (2015 to 2019), driven by long term trends of urbanisation, climate change, and asset value inflation.

- Geopolitical risk and US Political landscape There are three distinct shocks impacting the market through different transmission mechanisms. Firstly, the hot wars; the Russia-Ukraine war generated >$10 billion in aviation seizure losses (Guardian). Secondly, the supply chain blockers; the Houthi Red Sea campaign and subsequently the Iran actions on the Strait of Hormuz have repriced maritime war risks more than twenty-fold. Likewise, tariff uncertainty — US tariffs starting from 25% on steel and aluminum have an inflationary impact on property and motor claims costs by 15% to 25% (Swiss Re). Also, Lloyds have cautioned regarding potential inflation in building costs.

What can insurance carriers do?

The insurance market has entered a soft market phase more rapidly than previous cycles. However, the underlying risk environment has not softened. The carriers that navigate this phase most effectively will be those that maintain discipline, invest in rigorous reserving processes, demonstrate effective controls and risk management. These actions will also enable auditors, regulators, policyholders and investors to have confidence that the business is well managed.

- Maintain reserving rigor and effective controls. Analyse the forward-looking loss trends, particularly social inflation and climate-adjusted catastrophe expectations.Stress test reserves at the class level as aggregate adequacy can mask significant deterioration. Analyse class by class to prior-year development.

- Plans should be based on realistic grounded assumptions that reflect long-term trends. Manage expenses cautiously, grow in portfolios with sustainable profitability.

- Focus on risk management, capital management and reporting. Model the capital cycle – a major loss event could rapidly deplete surplus capital and reverse the competitive dynamic. Ensure capital model assumptions regarding future profitability are realistic.

- Demonstrate underwriting discipline and protect terms and conditions. Hard-market structural improvements – higher attachment points, tighter wordings – are as important as headline rate levels.

PKF Littlejohn’s insurance actuarial team works with carriers, managing agents, and Lloyd’s syndicates on reserving analysis, pricing and underwriting reviews, board-level reporting and training. For further information, please contact the insurance team.