In spite of healthy profits and available external capital, some insurance intermediaries still fall foul of the FCA’s regulatory capital requirements. Why does this happen and what can intermediaries do to prevent it?

Insurance intermediaries are profitable cash generating businesses with healthy margins. It’s one of the reasons why the industry has been ripe with M&A activity and attracted the interest of capital in the form of both private equity and private credit institutions.

So, bearing in mind the healthy profits and available external capital, why do numerous insurance intermediaries fall foul of the FCA’s regulatory capital requirements?

Why regulatory capital matters

Ensuring intermediaries have sufficient regulatory capital is important to absorb unexpected losses and reduce the risk of detriment to underlying clients in the market.

There are a multitude of reasons why firms fall short of their regulatory capital requirements including one off exceptional costs, excessive dividend extractions, large intangibles, swing commission arrangements and external debt to fund growth and early-stage losses. Many of these reasons can be put down to one thing: unsuitable company structure.

In the excitement of starting a business, intermediaries can often overlook the importance of future proofing their company structure. It is common for a company’s strategy to evolve over its lifecycle. Intermediaries may start to explore alternative ventures or approaches to their existing operating models that were never on the radar when they initially started. And that’s understandable, business is flexible and the insurance intermediary landscape is ever-evolving.

A simplistic structure

Despite the profitability and margins associated with mature insurance intermediaries, the start-up phase can be very different. Intermediaries often incur losses as they establish their offering and presence in the market.

This applies especially when they rely on proprietary technology to establish an advantage. This is not unusual, but it can erode regulatory capital headroom. If most of the funding has been obtained via debt with the equity funding only covering the minimum, this can lead to further erosion.

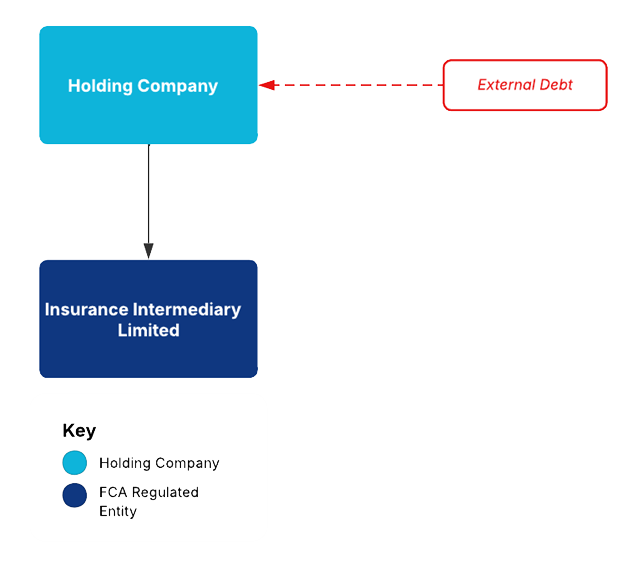

So what might be the solution? Incorporating a simple holding company, as seen in Illustration 1, to hold key debt arrangements can help to mitigate this impact on the minimum regulatory requirements.

Illustration 1: Start up structure

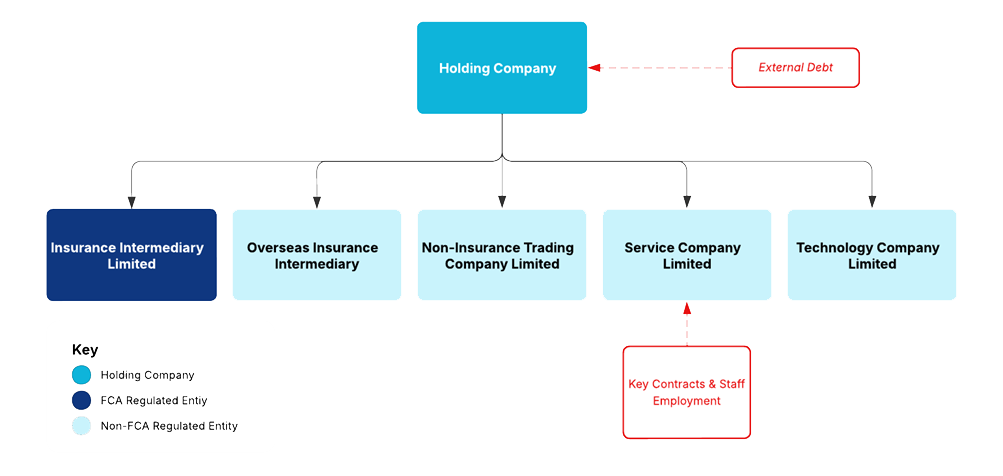

Whilst this initial structure may appear simplistic, it provides greater flexibility for the future as the company grows, matures and diversifies. For example, it may later establish other entities such as an overseas insurance intermediary and service company as seen in Illustration 2.

Illustration 2: Mature group structure

As well as assisting in maintaining regulatory capital, the flexibility and benefits include, but are not limited to:

- Centralised management and streamlined operations through the establishment of common service companies where key contracts and staff are employed.

- Separation of assets and liabilities helping to segregate and minimise the risk to the regulated entity.

- M&A activity and expansion including book purchases and diversification through the pre-established holding company, avoiding recognition of high debt levels and disallowable intangibles on the regulated entity’s balance sheet.

- International expansion through overseas subsidiaries which can be separated from existing regulated entities.

- Tax efficiencies including tax free intra-group dividends, tax neutral intra group asset transfers, sharing of tax losses between group members, VAT efficiencies and potential exemption from tax on the future sale of trading subsidiaries.

But is it really that simple?

Unfortunately, it isn’t necessarily that easy to meet regulatory capital requirements – and it shouldn’t be considering the importance of the insurance intermediary sector to the financial resilience of so many.

Firms must also ensure compliance with the FCA’s Threshold Condition 2.4 (“TC 2.4”), not solely their minimum capital requirement as reported in their Retail Mediation Activities Return. TC2.4 requires firms to maintain adequate financial (capital and liquidity) and non‑financial resources under both business‑as‑usual and wind‑down scenarios. Consequently, wind‑down planning is a key process for assessing whether additional capital or liquidity is required.

On paper, a regulated insurance intermediary may meet its minimum regulatory capital requirements through a simple holding company and shifting intangibles, debt and other liabilities off its balance sheet. But there are other risks and factors that need to be considered as part of overall FCA TC 2.4 compliance and the wind down assessment.

These include group reliance and interconnectedness. This is especially true where external debt is held by other group companies which may have guarantees and securities over the regulated entity and an inherent reliance to service this debt.

Intercompany debtors and associated recoverability in the scheme of regulatory capital is important and often overlooked. This particularly applies where the regulated entity is helping to fund operations elsewhere in the group.

This interconnectedness can increase the risk of failure and provide a false confidence for regulated entities who may quickly identify via their wind down plan assessment that they don’t have as much regulatory capital headroom as initially thought.

Early structuring decisions pay off

All these factors can be a lot to consider for insurance intermediaries, especially when starting their business. But early thoughts on a firm’s structure can provide future flexibility. It can help avoid headaches further down the line associated with restructuring which can be costly, shifting focus and resources away from what really matters for an intermediary.

How we can help

Whether you are setting up your business for the first time, or a larger corporate wanting to streamline your group whilst ensuring sufficient regulatory capital, we can provide advice on the appropriate structure for you now and for the future. Get in touch with Christopher Stout, or Michael Marslin in our Financial Accounting Advisory team to see how we can help.