SICR is a core driver of how credit risk is reflected in financial statements. For non‑bank lenders, staging decisions increasingly attract scrutiny from auditors, boards and regulators, particularly in periods of economic uncertainty.

While IFRS 9 provides flexibility, that flexibility must be underpinned by clear logic, forward‑looking insight and robust evidence. Frameworks that rely too heavily on arrears or mechanical triggers often fail to identify deterioration early and are difficult to defend when challenged.

Our Non-Bank Lending team work with some of the largest and fastest‑growing lenders in the UK and Europe to strengthen SICR frameworks, reduce noise in expected credit loss (ECL) models, and improve audit outcomes. This article explains the core problems many lenders face and the practical steps to fix them.

Why lenders should focus on SICR

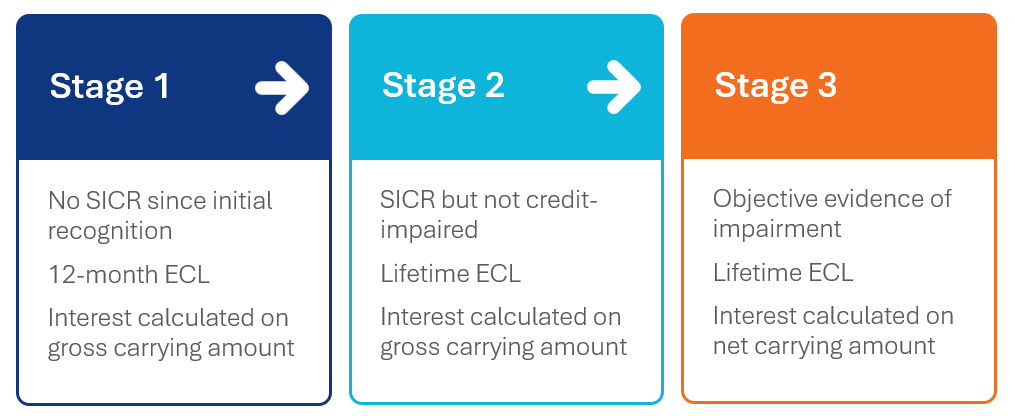

Under IFRS 9, the SICR assessment determines whether exposures remain in Stage 1 or move to Stage 2. That single decision shifts provisioning from a 12‑month to a lifetime ECL basis and can be the most material driver of impairment for portfolios with short maturities or rapidly changing risk profiles.

Common issues we see in practice include:

- thresholds that are either too sensitive or too blunt

- staging frameworks driven almost entirely by days‑past‑due (DPD)

- limited use of qualitative or forward‑looking information

- overrides that are poorly documented or inconsistently applied

- staging outcomes that don’t align with observed risk.

A well‑designed SICR framework is essential for stable provisioning, strong governance and credible financial reporting.

What a robust SICR framework looks like

A strong SICR framework doesn’t need to be complex. It needs to be purposeful, explainable, and grounded in how credit risk actually behaves.

- Clear quantitative triggers

Use a small number of intuitive metrics, with a demonstrable link to early deterioration such as:

- relative increases in PDs;

- deterioration from origination scores; and

- internal rating movements.

Critically, thresholds should be backtested to show they identify deterioration before arrears emerge, not after.

- Decisive qualitative indicators

Qualitative information often highlights risk earlier than models. Effective frameworks include:

- covenant breaches;

- restructuring activity or forbearance activity; and

- adverse changes in financial performance or sector outlook.

In practice, many lenders operate with no qualitative flags, even though they routinely observe clear signs of borrower stress in their day‑to‑day credit management. These indicators should be capable of triggering SICR independently, with clear documentation of the judgement applied.

- A well‑used backstop

IFRS 9’s 30‑DPD presumption should act as a safety net, not the primary SICR trigger. However, rebuttals should be rare, well‑documented and consistent with observed behaviour.

- Forward‑looking information that affects staging

Macroeconomic scenarios should influence staging where they materially change expectations of credit risk, not just when changes are observed in behaviour. We often encounter frameworks where scenarios influence PDs but have no impact on SICR decisions whatsoever. Forward‑looking inputs typically should not only affect ECL but also staging where appropriate.

- Strong, transparent governance

Effective SICR governance typically includes:

- clear ownership across Risk and Finance functions;

- documented policies and override approvals;

- ongoing performance monitoring against outcomes; and

- validation checks that explain actual outcomes.

Transparency is more important than complexity: if decision‑makers cannot articulate how staging works and why, the framework will struggle under scrutiny.

Practical steps for non‑bank lenders

Many SICR issues stem from design and governance rather than data availability. Lenders can strengthen their framework through:

- simplifying and rationalising indicators

- re‑testing thresholds using historic outcomes and scenario paths

- refining qualitative indicators to reflect borrower‑specific behaviour

- tightening override and rebuttal documentation

- enhancing internal challenge.

These changes result in stronger staging decisions, fewer audit issues and more stable impairment outcomes.

How we can help

SICR is not about perfect prediction. It’s about applying judgement in a controlled and evidence-based way that reflects real credit behaviour.

Our Non-Bank Lending team has experience supporting UK and European lenders to design, review and enhance SICR frameworks. We work across the full lifecycle, from independent assessments of methodology and thresholds, through to implementation support and audit readiness, helping firms achieve more stable provisioning, fewer audit challenges, and better insight into emerging risk.