The downward spiral continues

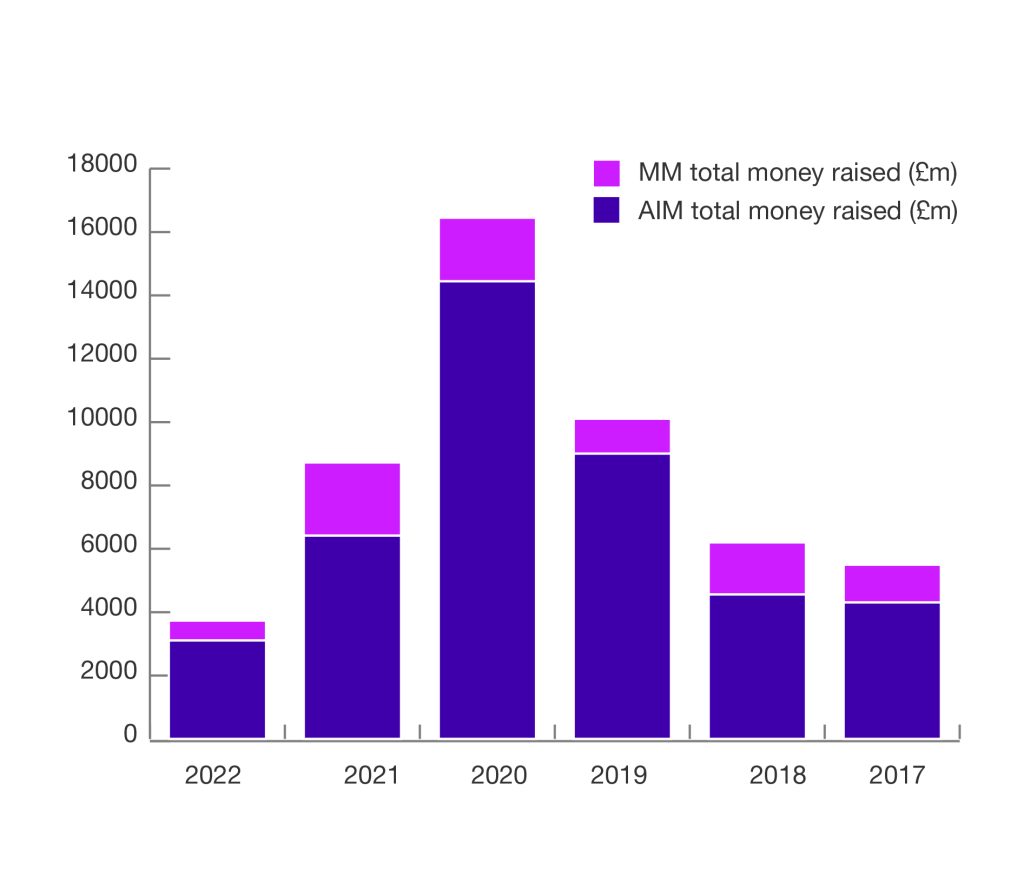

The quarter to June 2022 saw a total amount raised through new and further issues of £3.7 billion across AIM and the Main Market (compared to £8.7 billion in Q2 2021). The downward trend began in 2020 (Q2: £16.5 billion). The 2020 figure represents the most raised in the equivalent periods of the last five years, with a backdrop of paused, deferred and cancelled transactions, as investor appetite has declined.

Activity was down further on the comparative periods in 2018 and 2017. This was driven largely by the ongoing conflict, as well as surging hikes in interest rates and soaring inflation.

There was a total of three issues on AIM, including a new company placing, a reverse takeover and a main market transfer, and 10 on the Main Market. New issues in the second quarter raised £6 million (compared to Q2 2021: £298 million) on AIM and £202 million (Q2 2021: £1.9 billion) on the Main Market.

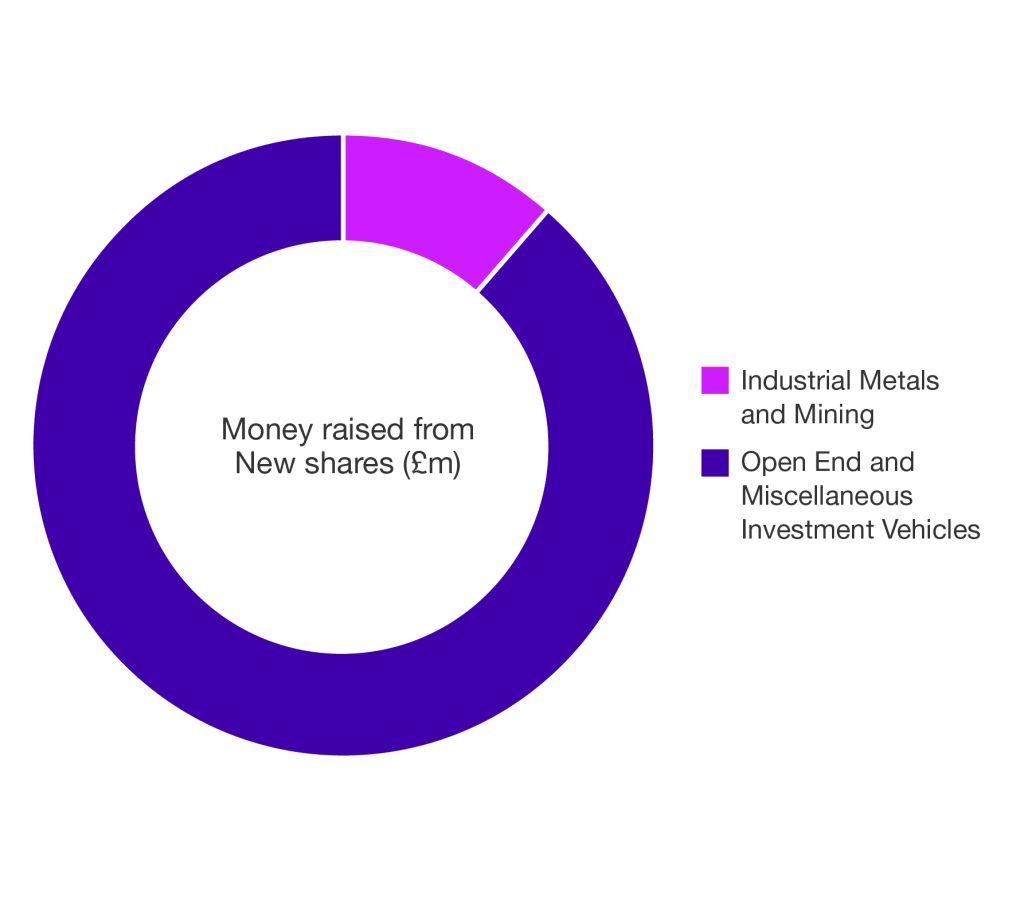

On the Main Market, the vast majority (£179 million) was raised by open end and miscellaneous investment vehicles, accounting for seven of the 10 new issues.

Main Market new issues included Financial Acquisition Corp, which raised £155 million in April 2022. There was also First Tin Plc, which successfully raised £20 million in the same month to accelerate its growth in sales of industrial metals and mining.

Financial Acquisition Corp, a special purpose acquisition company (SPAC) focused on insurance technology, was also the largest IPO in Q2, accounting for around 76% of total new issue money raised on the Main Market in the quarter. PKF was pleased to have acted as Reporting Accountant for Financial Acquisitions Corp, with a placing of 15,450,000 ordinary shares and 7,500,000 whole warrants at an issue price of 10 pounds per share.

Outlook – H2 and beyond

The macro-economic environment is driving down investor appetite markedly. The Bank of England’s increase in base rates, coupled with a cost-of-living crisis and the ongoing war in Ukraine, means there’s little optimism that this will pick up in the immediate future.

That said, we continue to see companies preparing to IPO, albeit at a slower rate. And it may be that some of these IPOs are deferred into 2023, with certain sectors such as energy weathering the storm.

Ultimately, the IPO market will not rally until broader capital markets stabilise and become less volatile. We are therefore seeing companies instead focus on the path to IPO, as increased scrutiny on IPO readiness continues in the interim period.

For more on IPOs, read our Preparing for an IPO: a brief guide article in this issue.